As you may have heard Brexit occurred two weeks ago and had large effects on the market. For a few days following the announcement, all the markets tanked a few percent every day all over the world. Having a position on at that time was nerve-wracking even though it was only a dummy position. I have many updates to record from the past two weeks that I will share with you below:

June 24th: On this day, I had to move my butterflies down to 1100 from 1120 in order to cope with Brexit repercussions.

June 27th: With the market tanking today, I moved all of my butterflies down to 1060. Now the position is at approximately 30 points below the market and is down about $1,000.

June 28th: Today I added the verticals 1080/1100 as well as moved half of my butterflies to 1080 in order to correct the positive Vega and negative Delta of the position. With the move, the Delta became -30 and the Vega returned to a negative value.

June 29th: I had to move the rest of the 20 butterflies up to 1080 because the Delta value had reached 24 which is a higher value then is what is recommended for the M3 position. Also, the Vega had turned positive again which was corrected with the movement of the butterflies.

June 30th: With yet another move up, I had to move all 20 of the butterflies to 1120 (30 points below the market position of 1150). At this point, the market is closer to the call than it was to the butterflies (before I adjusted them) and the Theta of the position became negative while the Vega of the position became positive. I also had to add the five verticals 1100/1130 because the negative Delta value was too high.

July 1st: The market only moved up 4 points today so it allowed the position to gain a little bit of the positive Theta but since the Gamma was negative and significant, I had to add the verticals 1130/1150 to keep the negative Delta within limits.

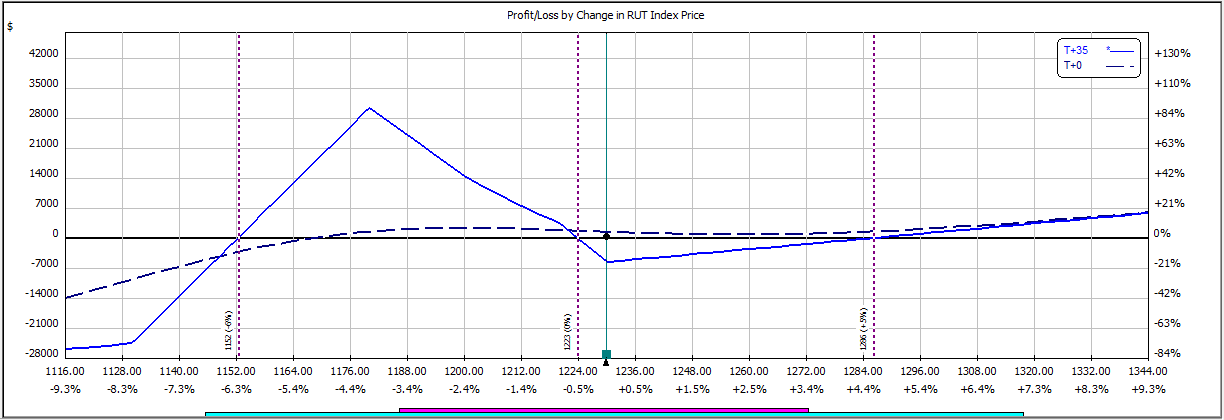

July 5th: I finally took the position off today with only ten days until expiration. Even though throughout a majority of the trade I was at a loss, at the end I made a profit of $1,483. I decided to take the position off because the Delta was very high and adjusting it again might risk the profit.

The final risk profile chart for this month can be seen below: