Originally, I had planned to put on my June position at 56 days until expiration which is recommended for the position but I only just got around to it. I put the position on through BackTrader on Friday (49 DTE) which was down about nine points and at about 1130. Following the 20-30 points rule, I put on my butterflies at 1100 (being more worried about the backside than the front). I also bought a call at 1000 with a Delta of 90. When I put on the position, I also had to put on a vertical to balance the Delta since you shouldn't buy a call that is too far in the money (problems with extrinsic value).

The risk profile graph from Friday can be seen below:

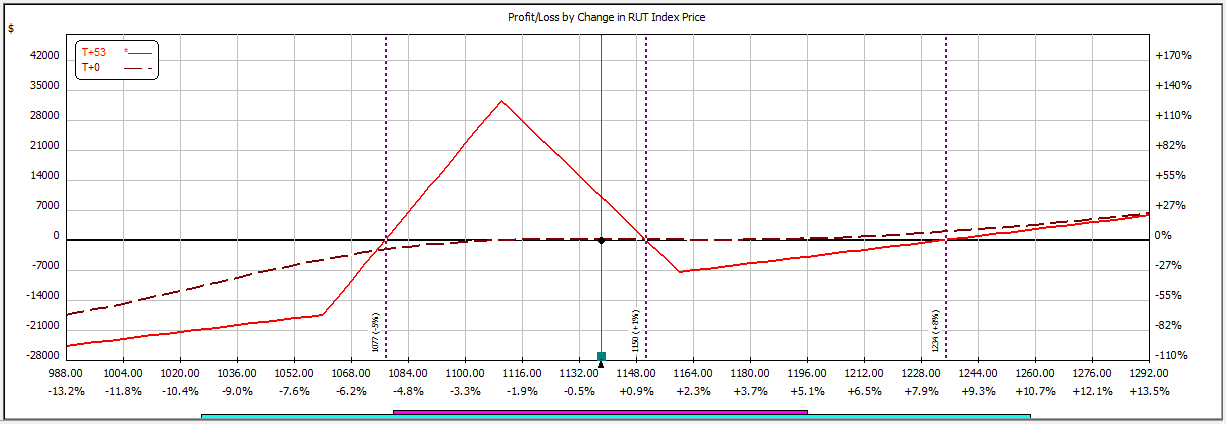

The position needed no adjusting until yesterday when the market moved back significantly and the Delta value became 18. Since the limit for positive Delta is 20, I found the value a bit too close for comfort and decided to move the butterflies down. It was not a significant shift, only 10 points, to adjust the butterflies to 1090. With this shift, the Delta was only 3 and was not as large of a concern. As of today, the position is up about $601 and the Greeks of the position are as follows: Delta 7.28, Theta 108, Gamma, -2, and Vega is -478 (bad for the position recently because the market has been down causing the volatility to rise but since the position has a negative value, it inflicts damage).

The current risk profile graph can be seen below: